New Property vs. Old Property Depreciation Difference

When it comes to property investing, one big question always pops up — should you buy new or go for old? It’s not just about location or price, hey. The age of your property plays a major role in how much you can claim in tax depreciation. And that can make a real difference to your cash flow.

Whether you’re eyeing a sleek, modern apartment or a fixer-upper with potential, understanding the depreciation differences between new and old properties is key to making the right investment move.

Some people prefer to invest in brand-new properties while others opt for older properties that they can renovate and resell for profit. So, which is the better investment strategy? New vs old property?

What’s the difference in depreciation for new and old properties?

When it comes to maximising your deductions, the age of your property can make a big difference to your tax return. You can explore our practical investment property depreciation tips.

New properties often come with greater depreciation benefits, while older properties can be a bit more complex. However, that doesn’t mean they’re not worth claiming! The key is understanding how depreciation rules apply differently to new vs old builds — so you can make the most of every deduction you’re entitled to.

Let’s have a look at some of the pros and cons of buying brand-new properties and almost-new properties. Many investors discover that new property depreciation benefits play a key role in improving cash flow.

Buying new property will help investor cash flow due to greater tax depreciation benefits. Property tax depreciation benefits are at their greatest when the property is brand-new. With brand-new property you maximise your available property tax deductions which adds a significant boost to your cash flow position.

Depreciation allowances for new properties can yield big tax breaks. Investors can claim a 2.5% depreciation allowance on the construction cost of new property. Plus you’ll also be entitled to claim the full amount of depreciation allowances on plant and equipment items, such as blinds, ovens, carpets and air-conditioners, which will all be brand new.

By way of example, the owner of a brand-new property, Melbourne, high-rise unit recently purchased for $440,000, was able to claim $12,000 in depreciation in the first year.

View the video below to learn more about how new property can lead to thousands more in depreciation deductions, when compared to older properties.

Work out how much you save using our free property depreciation calculator or make it happen and get an obligation free quote

Maximise your cash flow

How the property depreciation changes affect buying brand new property versus second hand property.

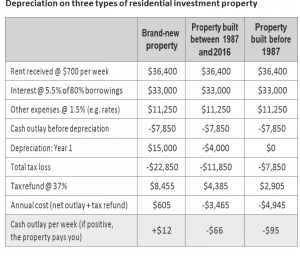

Let’s look at this in actual finite depreciation details. If you look at depreciation Table 5.1 below, you’ll see the net effect of the cost of owning a property broken down into three examples:

• a brand-new property;

• a property built between 1987 and 2024; and

• a property built before 1987.

The middle column highlights that the property is second-hand and you will be acquiring previously used assets if you purchase it now.

The depreciation assumptions are the same for every property: each one will generate a weekly rental income of $700 over a 52-week period, which works out at $36,000 per property.

Furthermore, the interest rate is 5.5 per cent on each property on borrowings of 80 per cent of the purchase price – that’s an annual interest bill of $33,000 which is the same to illustrate the net effect on depreciation property.

Each depreciating property will have other expenses at 1.5 per cent of the purchase price, which makes $11,250 annually for each property. Now, you could argue that property built before 1987 could have higher expenses, but for ease of comparison we’ve kept the same rate.

So, it’s the same depreciating scenario for each property with the net outlay before depreciation of $7,850.

Now, here’s where things get interesting, what about the property depreciation?

- In a brand-new property, the depreciation in year one is

$15,000; - For the property built between 1987 and 2024, it’s $4,000 because all you claim there is the structure of the building; and

- For a property built before 1987, the depreciation is $0.

Depreciation on a brand-new property

You can see that the total tax loss on the brand-new property is quite high at $22,850. If you are an investor who is paying tax at a marginal tax rate of 37.5 per cent and you’re making a loss of $22,850, you will receive a tax cheque back from the ATO to the tune of $8,455 – and that’s cash in hand. According to the ATO, investors may be able to claim deductions for depreciating assets, which play a key role in maximising these benefits.

However, you have physically paid out $7,850, remember? You’ve been paying $605 a year to own that property – so the net return is $12 a week positive cash flow.

Depreciation on an old property

Next, let’s look at the property built before 1987. Again, you have physically paid out $7,850 over the year to hold the property. You can’t claim any depreciation on your investment, so the total tax loss continues to be $7,850. If you are in the 37 per cent income tax bracket, there will be a tax return of $2,905.

Given that $7,850 has been paid out and there’s a tax cheque of

$2,905, it’s cost you roughly $5,000 per year to own. That’s just under $100 per week to own a property built before 1987.

Depreciation on a second-hand property built between 1987 and 2024

Using the same variables, if you bought a property built between 1987 and 2024, your annual tax loss would be $11,850, so you would receive a tax refund of $4,385 (providing you are in the 37 per cent bracket). Your cash outlay was $7,850, so your annual cash outlay is $3,465. That means your weekly cash flow is negative $66, but you’ll still eventually realise a capital gain over the medium to long term. You can review a sample depreciation report for older properties to see how these figures are typically presented.

As you can see, there are depreciating pros and cons of buying brand-new and almost-new properties, depending on your investment strategy.

Furthermore, buying brand-new property often carries the developer’s profit, which you pay for in the purchase price. If you buy something ‘newish’ – say a five to ten-year-old property – there is a fair chance that it has been bought and resold a few times. Therefore the value is now reflected in a more realistic way on the open market.

Work out how much you save using our free property depreciation calculator or make it happen and get an obligation free quote for a depreciation schedule now.