What is Capital Gains Tax (CGT)?

Capital gains tax (CGT) is a tax levied on the profit from selling an asset, such as an investment property. In Australia, the CGT is calculated based on the difference between the purchase cost and the sale price and is generally payable by the person who disposed of the asset.

To ensure you understand just how capital gains tax can affect your investment property in Australia, we’ve broken it down in this blog post.

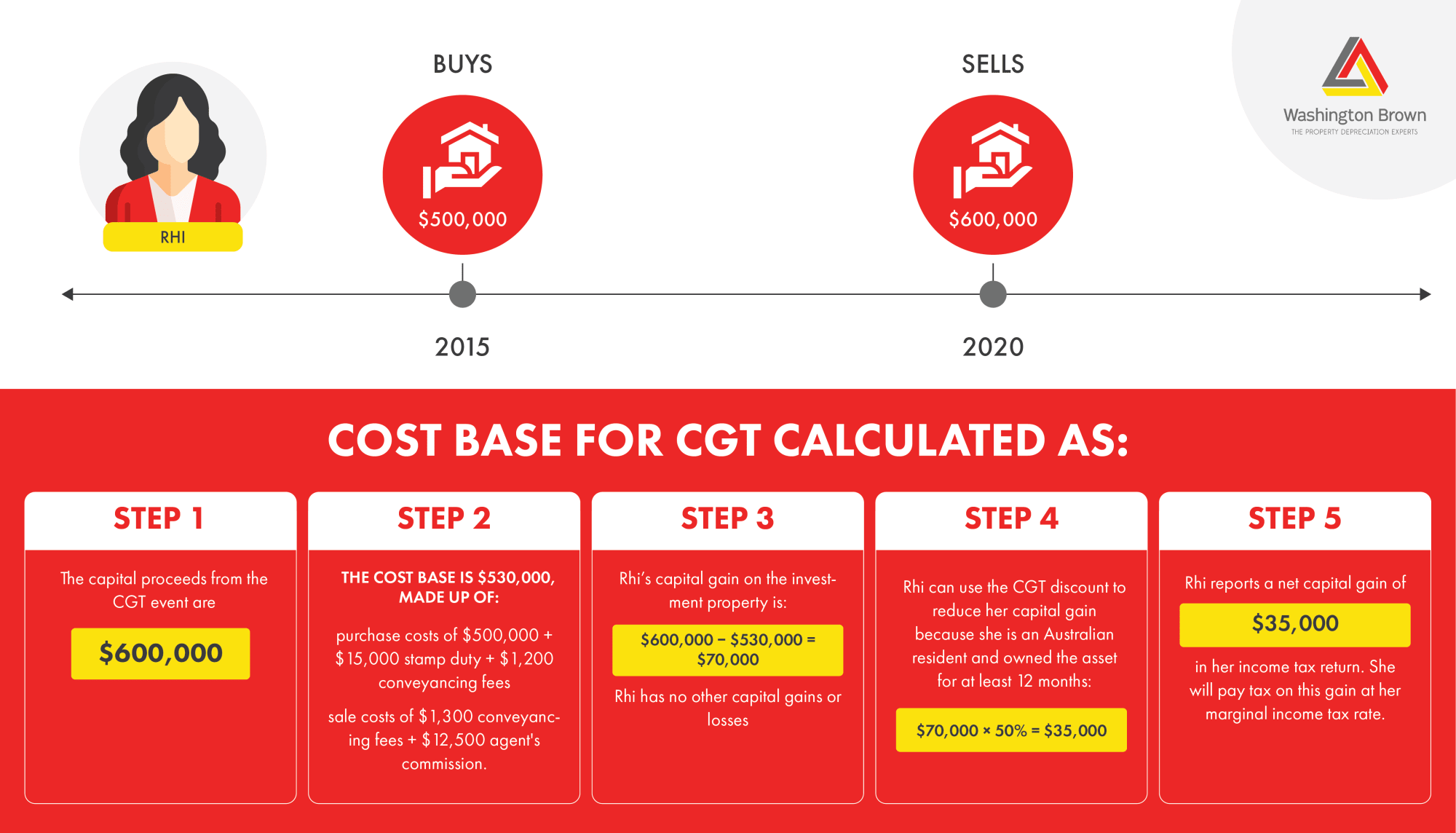

Below is an example on how Rhi calculated CGT for a property that she purchased for $500,000 in 2015 and then sold for $600,000 in 2020.

Steps for Calculating CGT on an Investment Property in Australia

- Determine the Cost Base of the Property

The CGT is calculated based on the difference between the purchase costs. The cost base is the sum of the total costs of the property, including the purchase price, stamp duty, legal fees, and other costs associated with acquiring, holding and disposing of the property.

It is essential to keep accurate records of these costs, as they will be used to calculate the CGT.

- Determine the Capital Gain or Loss

The next step is determining the capital gain or loss made on the sale of the property. This is done by subtracting the property’s cost base from the sale price.

If the sale price is greater than the cost base, a capital gain has been made, and if the sale price is less than the cost base, a capital loss has been made.

- Apply the Relevant CGT Rate

Once the capital gain or loss has been determined, applying the relevant CGT rate is necessary. The CGT rate in Australia varies for individuals.

- Apply the CGT Discount (if applicable)

If you are eligible for the 50% CGT discount, apply it to your capital gain:

Discounted Capital Gain = Capital Gain × 0.5

In our example, Rhi can use the CGT discount to reduce her capital gain as she is an Australian tax resident and owned the asset for at least 12 months.

- Include the Net Capital Gain (or Loss) in Your Tax Return

The next step is calculating the actual CGT amount by multiplying the capital gain or loss by the relevant CGT rate. If a capital gain has been made, the CGT amount will be added to the individual’s taxable income for the financial year in which the sale occurred.

If a capital loss has been made, the CGT amount can be offset against any capital gains made in the same financial year.

Key Factors to Consider When Calculating CGT

However, there are some situations where a different rate may apply, such as if the property has been held for more than 12 months and is eligible for the CGT discount.

It is important to note that some exemptions and concessions are available for CGT on investment properties in Australia. For example, if the property was used as the individual’s primary residence for at least some time that they owned it, they may be eligible for the main residence exemption. This means that no CGT will be payable on the sale of the property.

Additionally, suppose an individual is over 55 years of age, and they sell their home. In that case, they may be eligible for the downsizing contributions measure, which allows them to contribute up to $300,000 of the proceeds from the sale of their home into their superannuation account.

Calculating CGT on an investment property in Australia involves determining the property’s cost base, determining the capital gain or loss made on the sale of the property, applying the relevant CGT rate, and calculating the actual CGT amount.

It is essential to keep accurate records of all costs associated with the property and to be aware of any exemptions and concessions that may apply. It’s always advisable to consult with a tax professional or accountant for a clearer understanding of your tax situation and to ensure you comply with the tax law.

I believe every year millions of dollars get paid in Capital Gains Tax that shouldn’t be, and here’s why:

When people renovate a property they are living in – they rarely keep records of their cost incurred on the upgrades that they make.

Then a baby might come along, a work opportunity overseas or any other reason that forces the property owner to turn that owner occupied property into an investment property.

Let’s move on 5 or 10 years… the owners decide to sell the property.

Managing CGT Implications as a Property Investor

NOW because the property has been partially owner occupied and partially an investment – A Capital Gain Tax (CGT) implication has been triggered.

So off they go to their accountant – and the accountant asks “have you got any receipts of what work you did to the property??? Because that will REDUCE the CGT Payable“

You see any improvements the couple made to the property whilst living there, INCREASES the cost base of the property – thus lowering the amount you will need to pay in CGT.

We are increasingly being asked by accountants to go to a property to estimate the improvements made or in some cases the whole construction cost.

See a sample depreciation report to understand how estimating renovation costs can help increase your cost base and lower the tax you pay.

How To Avoid Paying Capital Gains Tax

There are several ways to avoid paying capital gains tax when selling property in Australia, including:

- Living in the property as your primary residence: If you live in the property as your primary residence for at least six months of the year, you may be eligible for a full exemption on the capital gains tax.

- Using the property as an investment: If you rent it out, you can claim deductions for expenses such as repairs, property management fees, interest on the mortgage, and even a rental property depreciation. These deductions can offset capital gains, reducing the tax you have to pay. However, if such costs are claimed while the property is an investment, they can’t also be used to reduce the cost base.

- Using the property in a business: If you use the property in a business, such as a bed and breakfast or a farm, you may be eligible for a reduced rate of capital gains tax.

- Using the downsizer contribution: If you are over the age of 55 and sell your home, you may be eligible to make a downsizer contribution of up to $300,000 from the proceeds of the sale into your superannuation.

It’s important to consult a financial advisor or tax professional to determine which strategy is best for you.